[Updated 1 December 2017 with reissued Place of Work data]

The ABS has now released all census data for the 2016 journey to work. This post takes a city-level view of mode share trends. It has been expanded and updated from a first edition that only looked at place of work data.

My preferred measure of mode share is by place of enumeration – ie how did you travel to work based on where you were on census night (see appendix for discussion on other measures).

I’m using Greater Capital City Statistical Areas (GCCSA) geography for 2011 and 2016 and Statistical Divisions for earlier years. For Perth, Melbourne, Adelaide, Brisbane and Hobart the GCCSAs are larger than the Statistical Divisions used for earlier years, but then those cities have also grown over time. See appendix 1 for more discussion.

Some of my data goes back to 1976 – I’ll show as much history as I have for each mode/modal combination.

Public transport mode share

Sydney continues to have the largest public transport mode share, and the largest shift of the big cities. Melbourne also saw significant positive mode shift, but Perth and particularly Brisbane had mode shift away from public transport.

There’s so much to unpack behind these trends, particularly around the changing distribution of jobs in cities that I’m going to save that lengthy discussion for another blog post.

But what about the…

Massive mode shift to “public transport” in Darwin?!?

[this section updated 26 Oct 2017]

Yes, I have triple-checked I downloaded the right data. “Public transport” mode share increased from 4.3% to 10.9%. The number of people reporting bus-only journeys went from 1648 in 2011 to 5661 in 2016, which is growth of 244%. There has also been a spike in the total number of journeys to work in 2011, 30% higher than in 2011, while population growth was 13%.

Here’s the percentage growth in selected journey types between 2011 and 2016:

Bus + car as driver grew from 74 to 866 journeys, which reflects the establishment of park and ride sites around Darwin for the special commuter buses. Bus only journeys increased from 1953 to 5744. So it looks like most workers are getting the bus from home and/or forgot to mention the car part of their journey (in previous censuses I’ve seen many people living kilometres from a train station saying they got to work by train and walking only).

So this new project has swamped organic trends, although it is quite plausible that some people have shifted from cycling/walking to local jobs to using buses to commute to the LNG project (which is outside urban Darwin). When I look at workplaces within the Darwin Significant Urban Area (2011 boundary), public transport mode share is 6.0%, in 2016, still an increase from 4.4% in 2011. More on that in a future post.

Train

Sydney saw the fastest train mode share growth, followed by Melbourne, while Brisbane and Perth went backwards.

Bus

Darwin just overtook Sydney for top spot thanks to the LNG project. Otherwise only Sydney, Canberra and Melbourne saw growth in bus mode share. Melbourne’s figure remains very low, however it is important to keep in mind that trams provide most of the on-street inner suburban radial public transport function in Melbourne.

Train and bus

Sydney comes out on top, with a large increase in 2016 (although much of this is still concentrated around Bondi where there are high bus frequencies and no fare penalties for transfers – more on that in an upcoming post). Melbourne is seeing substantial growth (perhaps due to improvements in modal coordination), while Perth, Adelaide and Brisbane had declines in terms of mode share (Brisbane and Adelaide were also declines on raw counts, not just mode share). I’m sure some people will want to comment about degrees of modal integration in different cities.

Train and bicycle

Some cities are also trying to promote the bicycle and train combination as an efficient way to get around (they are the fastest motorised and (mostly)non-motorised surface modes because they can generally sail past congested traffic). The mode shares are still tiny however:

Sydney and Melbourne are growing but the other cities are in decline in terms of mode share.

As this modal combination is coming off an almost zero base, it’s also probably worth looking at the raw counts:

The downturns in Brisbane and Perth are not huge in raw numbers, and probably reflect the general mode shift away from public transport (which is probably more to do with changing job distributions than bicycle facilities at train stations).

Cycling

I have a longer time-series of bicycle-only mode share, compared to “involving bicycle”, so two charts here:

Observations:

Darwin lost top placing for cycling to work with a large decline in mode share (refer discussion above about the massive shift to bus).

Canberra took the lead with more strong growth.

Melbourne increased slightly between 2011 and 2016 (note: rain was forecast on census day which may have suppressed growth, more on that in a moment).

Hobart had a big increase in 2016, following rain in 2011.

Sydney remains at the bottom of the pack and declined in 2016.

Walking and cycling mode share is likely to be impacted by weather. Here’s a summary of recent census weather conditions for most cities (note: Canberra minimums were -3 in 2001, -7 in 2006, 0 in 2011 and -1 in 2016):

Perth had rain on all of the last four census days, while Adelaide had significant rain only in 2001 and 2011 (and indeed 2006 shows up with higher active transport mode share). Hobart had significant rain in 2011, which appears to have suppressed active transport mode share that year.

But perhaps equally important is the forecast weather as that could set people’s plans the night before. Here was the forecast for the 2016 census day, from the BOM website the night before:

Note that it didn’t end up raining in Melbourne, Adelaide, or Hobart.

The census is conducted in winter – which is the best time to cycle in Darwin (dry season) and not a great time to cycle in other cities. However the icy weather in Canberra clearly hasn’t stopped it getting the highest and fastest growing cycling mode share of all cities!

Indeed here is a chart from VicRoads showing the seasonality of cycling in Melbourne at their bicycle counters:

And in case you are interested, here are the (small) mode shares of journeys involving bicycle and some other modes (other than walking):

Walking only

Canberra was the only city to have a big increase, while there were declines in Darwin, Perth, Adelaide, Brisbane, and Sydney.

The smaller cities had the highest walking share, perhaps as people are – on average – closer to their workplace, followed by Sydney – the densest city. But city size doesn’t seem to explain cycling mode shares.

Car

The following chart shows the proportion of journeys to work made by car only (either as driver or passenger):

Sydney has the lowest car only mode share and it declined again in 2016. It was followed by Melbourne in 2016. Brisbane and Perth had large increases in car mode share in 2016 (in line with the PT decline mentioned above). Darwin also shows a big shift away from the car to public transport (although the total number of car trips still increased by 24%). Adelaide hit top spot, followed by Hobart and Perth.

Here is car as driver only:

And here is car as passenger only:

Car as passenger declined in all cities again in 2016, but was more common in the smaller cities, and least common in the bigger cities. I’m not sure why car as passenger declines paused for Perth and Sydney in 2006.

We can calculate an implied notional journey to work car occupancy by comparing car driver only and car passenger only journeys. This is not actual car occupancy, because it excludes people not travelling to work and excludes journeys that involved cars and other modes. However it does provide an indication of trends in car pooling for journeys to work.

There were further significant decreases in car commuter occupancy, in line with increasing car ownership and affordability.

Private transport

Here is a chart summing all modal combinations involving cars (driver or passenger), motorcycle/scooter, taxis, and trucks, but excluding any journeys that also include public transport.

The trends mirror what we have seen above, and are very similar to car-only travel.

Overall mode split

Here’s an overall split of journeys to work by “main mode” (click to enlarge):

Note: the 2001 data includes estimated splits of aggregated modes based on 2006 data.

I assigned a ‘main mode’ based on a hierarchy as follows:

Any journey involving train is counted with the main mode as train

Any other journey involving bus is counted with the main mode as bus

Any other journey involving tram and/or ferry is counted as “tram/ferry”

Any other journey involving car as driver, truck or motorbike/scooter is counted as “vehicle driver”

Any other journey involving car as passenger or taxi is counted as “vehicle passenger”

Any other journey involving walking or cycling only as “active”

How different are “place of work” and “place of enumeration” mode shares?

[this section updated 1 December 2017 with re-issued Place of Work data. See new Appendix 3 below for analysis of the changes]

The first edition of this post reported only “place of work” data, as place of enumeration data wasn’t released until 11 November 2017. This second edition now focuses on place of enumeration – where people were on census night.

The differences are not huge, as most people who live in a city also work in that city, but there are still a number of people who leave or enter cities’ statistical boundaries to go to work. Here’s an animation showing the main mode split by place of work and enumeration so you can compare the differences (you’ll need to click to enlarge). The animation dwells longer on place of work data.

Public + active transport main mode shares are generally higher for larger cities with place of work data, and smaller for smaller cities.

Here’s a closer look at the 2016 public transport mode shares by the two measures:

See also a detailed comparison in Appendix 1 below for 2011 Melbourne data.

I’d like to acknowledge Dr John Stone for assistance with historical journey to work data.

Appendix 1 – How to measure journey to work mode share

Firstly, I exclude people who did not work, worked at home, or did not state how they worked. The first two categories generate no transport activity, and if the actual results for “not stated” were biased in any way we would have no way of knowing how.

I prefer to use “place of enumeration” data (ie where people were on census night). “Place of usual residence” data is also available, but is unfortunately contaminated by people who were away from home on census day. The other data source is “Place of work”.

Some people might prefer to measure mode shares on Urban Centres which excludes rural areas within the larger blobs that are Greater Capital City Statistical Areas and Statistical Divisions (use this ABS map page to compare boundaries). However, “place of work” data is not readily available for that geography, and this method also excludes satellite urban centres that might be detached from the main urban centre, but are very much part of the economic unit of the city.

Another option is “Significant Urban Area”, which includes more fringe areas, and some more satellite towns, and in Canberra’s case crosses the NSW border to capture Queanbeyan.

What difference does it make?

Here’s a comparison of public transport mode shares for the different methods for 2011.

If you look closely, you’ll notice:

The more than you remove non-urban areas, the higher your public transport mode share, which makes sense, as those non-urban areas are mostly not served by public transport.

Place of usual residence tends to increase public transport mode shares for smaller cities (people probably visiting larger cities) and depresses public transport mode share in larger cities (people visiting smaller cities and towns).

Place of work is only readily available for Greater Capital City Statistical Areas. For the bigger cities it tends to inflate PT mode share where people might be using good inter-urban public transport options, or driving to good public transport options on the edges of cities (eg trains). However it has the opposite impact in Darwin and Canberra, where driving into the city is probably easier.

But I think the main point is that for any time series trend analysis you should use the same measure if possible.

If you want to compare the two, I’ve created a Tableau Public visualisation that has a large number of mode shares by both place of work and place of enumeration.

Appendix 2 – Estimating pre-2006 mode shares from aggregated data

For 2006 onwards, ABS TableBuilder provides counts for every possible combination of up to three modes (other than walking, which is assumed to be part of every journey). For example, in Melbourne in 2006, 36 people went to work by taxi, car as driver, and car as passenger (or so they said!). Unfortunately for years before 2006 data is not readily available with a full breakdown.

The 2001 data includes only aggregated counts for the following categories:

train and other (excluding bus)

bus and other (excluding train)

other two modes (no train or bus)

train and two other modes

bus and two other modes (excluding train)

three other modes (no train or bus)

Together these accounted for 3.7% of journeys in Melbourne and 4.5% of journeys in Sydney.

However all but two of those aggregate categories definitely involve train and/or bus, so can be included in public transport mode share calculations.

Journeys in the aggregate categories “Other two modes” and “Other three modes” might involve tram and/or ferry trips (if such modes exist in a city), but we don’t know for sure.

I’ve used the complete modal data for 2006 to calculate the percentage of 2006 journeys that fit into these two categories that are by public transport. I’ve then assumed these same percentage apply in 2001 to estimate total public transport mode shares for 2001 (for want of a better method).

Here are the 2001 relevant stats for each city:

(note: totals do not add perfectly due to rounding)

The estimates add up to 0.2% to the total public transport mode shares in cities with significant modes beyond train and bus (namely ferry and tram in Sydney, tram in Melbourne, ferry in Brisbane, tram and Adelaide). This almost entirely comes from “other two modes” category while “other three modes” is tiny. For these categories, almost no journeys in Perth, Canberra and Hobart actually involved a public transport mode.

In the past I have knowingly ignored public transport journeys that might be part of these categories, which almost certainly means public transport mode share is underestimated (I suspect most other analysts have too). By including some assumed public transport journeys my estimate should be closer to the true value, which I think is better than an underestimate.

But are these reasonable estimates? Are the 2001 modal breakdowns for these categories likely to be the same as 2006? Maybe not exactly, but because we are multiplying small numbers by small numbers, the impact of slightly inaccurate estimates is unlikely to shift the total by more than 0.1%. I tested the methodology between 2006 and 2011 results (eg using 2011 full breakdown against created 2006 aggregate categories and vice versa) and the estimated total mode shares were almost always exactly the same as the perfectly calculated shares (at worst there was a difference of 0.1% when rounding to one decimal place).

In the first edition of this post I had to estimate 2016 place of work mode shares in a similar way for public and private transport, but I wasn’t confident enough to estimate mode share of journeys involving cycling.

I now have the final data and I promised to see how I went, so here’s a comparison:

If you round to one decimal place, the estimates were no different for public and private transport and out by up to 0.1% for cycling (which is relatively significant for the small cycling mode shares).

I’ve applied a similar approach to estimate several other mode share types, and these are marked on charts.

Appendix 3 – How different is the re-issued place of work data?

In December 2017, ABS re-issued Place of Work data due to data quality issues. This is how they described it:

**The place of work data for the 2016 Census has been temporarily removed from the ABS website so an issue can be corrected. There was a discrepancy in the process used to transform detailed workplace location information into data suitable for output. The ABS will release the updated information in TableBuilder on December 2. The Working Population Profiles will be updated on December 13.**

I have loaded the new data, and here are differences in public transport and private transport mode shares for capital cities:

You can see differences of up to 0.3% (Melbourne PT mode share), but mostly quite small.

Over one million private dwellings in Australia were unoccupied on census night in 2016 – 11.2% of all private dwellings – up from 10.2% in 2011.

This raises many questions. Where are these unoccupied dwellings and where are they now more prevalent? What type of dwellings are more likely to be unoccupied? How long have these dwellings been unoccupied? Do we know why these dwellings are unoccupied?

This post will focus on dwelling occupancy by geography, dwelling types and trends over time. In a future post I hope look into those last two questions in more detail.

I’ve prepared data for sixteen Australian cities, with various maps in Tableau (you will need to zoom and pan to your city of interest).

Why am I blogging about dwelling occupancy on a transport blog? Well partly because I’m interested in urban issues, but also because land use is very relevant to transport. If dwelling occupancy rates in the inner and middle suburbs were higher, there would be more people living closer to jobs and activities who might be less reliant on private motorised transport for their daily travel.

If you’d like to read more around the associated policy issues, Professor Hal Pawson from UNSW has a good piece in The Conversation highlighting the increasing number of empty properties and spare bedrooms, and advocates replacing stamp duty with a broad-based land tax to improve housing mobility. Also read Eryk Bagshaw in the Fairfax press, Jonathan Jackson in Finfeed, and a piece in Business Insider where the Commonwealth Bank state that 17% of recently built dwellings are left unoccupied (not sure how that was calculated).

What are the dwelling occupancy rates in Australian cities?

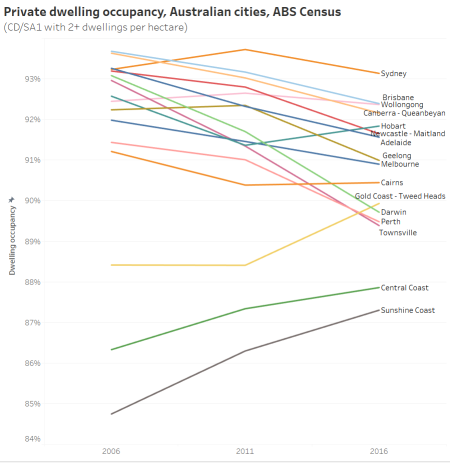

Here’s a chart showing private dwelling occupancy rates for sixteen Australian cities (using 2011 Significant Urban Area boundaries) from the last three censuses:

Note the y-axis only runs from 84% to 94%, so the changes are not massive. However a small change in dwelling occupancy can still have a large impact on housing prices (rental and sales).

The Sunshine and Central Coasts have the lowest occupancy, almost certainly explained by many holiday homes in those regions, although all three have been trending upwards. Curiously, the Gold Coast – Tweed Heads had a significant increase in occupancy between 2011 and 2016 to take it above Perth, Townsville, and Darwin.

Hobart and Cairns also had increased occupancy between 2011 and 2016, but all large cities declined between 2011 and 2016. Perth, Darwin and Townsville had big slides – quite possibly related to the downturn in the mining industry and slowing population growth (all three have seen slowing population growth in recent years after a boom period). Then again, if there are more fly-in-fly-out workers in a city you might expect dwelling occupancy on census night to go down as a portion of them will be away for work on census night.

How does dwelling occupancy in capital cities compare to the rest of the country?

Private dwelling occupancy is significantly lower outside the capital city areas. While the capital city areas contain 63% of all private dwellings, they only contain 51% of unoccupied private dwellings.

How does dwelling occupancy vary by dwelling type?

Here’s a chart of 2016 dwelling occupancy by Greater Capital City Statistical Areas and the most common dwelling types:

In many cities there is a strong correlation between housing type and occupancy, with separate houses having the highest occupancy rates, and multi-storey flats/apartments having the lowest. The pattern is strongest in Perth – perhaps reflecting reduced demand for apartment living following the end of the mining boom(?).

The data suggests higher density apartments are more likely to not be occupied on census night, but it doesn’t tell us why. Of course different dwelling types have different spatial distributions, so is it the dwelling type that drives the occupancy rates? I’ll come back to that shortly.

Where are the unoccupied dwellings?

Quite simply, here is a map showing the density (at SA2 geography) of unoccupied dwellings in Melbourne over time (you might need to click to enlarge to read more clearly):

(I’ve not shaded SA2s with less than 1 unoccupied dwelling per hectare. You can look at other cities in Tableau by zooming out and then in on another city).

You can see a fairly significant increase in the number of unoccupied dwellings in the inner and middle suburbs (at least at densities above 1 per hectare).

From a transport perspective – this isn’t great. If people lived in those dwellings rather than dwellings on the fringe of Melbourne, the transport task would be easier as there would be many more people living closer to jobs and other destinations with non-car modes being more competitive.

But these areas with a relatively high density of unoccupied dwellings are also areas with a high density of dwellings in general. The density of unoccupied dwellings has risen in the same places where total dwelling density has risen:

(see in Tableau – you may need to change the geography type)

Given you would expect a small percentage of dwellings to be unoccupied for good reasons (eg resident temporarily absent, or property on the market), it makes sense that the density of unoccupied dwellings has gone up with total dwelling density.

But a decrease in the dwelling occupancy rate requires the number of unoccupied dwellings to be growing at a faster rate than the total number of dwellings. We already know that is happening at the city level through declining occupancy rates, so how does that look inside cities?

How does dwelling occupancy vary across Melbourne?

Here’s a map of dwelling occupancy in Melbourne and Geelong at CD/SA1 level geography:

You can see very clearly that occupancy is lowest on Mornington Peninsula beaches to the south – which almost certainly reflects empty holiday homes on census night (a Tuesday night in winter).

In fact, I’ve created a map of dwelling occupancy at SA2 level for all of Australia, and you can see many coastal holiday areas around Melbourne (and other cities) with low occupancy (with Lorne – Anglesea at 32% and Phillip Island at 40%):

The previous Melbourne map at CD/SA1 level is very detailed and so it’s not easy to see the overall trends. Also, apart from the Mornington Peninsula, occupancy rates are almost all above 80%.

So here is a zoomed-in map with a different (narrower) colour scale, with data aggregated at SA2 level (also in Tableau):

Things become much clearer.

The highest dwelling occupancy is generally on the fringe of Melbourne.

Apart from holiday home areas, the lowest occupancy in 2016 was concentrated in wealthier inner suburbs, including Toorak at 83% and South Yarra west at 84%. This was closely followed by the CBD, Docklands, East Melbourne, Southbank, and Albert Park between 84% and 86%. These areas have all had declining occupancy since 2011.

It can be a little difficult to see the changes in occupancy rates, so here is a non-animated map the change in dwelling occupancy rates between 2006 and 2016 (also in Tableau):

There are at least small declines in most parts of Melbourne. The biggest decline was 7% in Bundoora North (with lowest 2016 occupancy of 79% in these new units in University Hill ), followed by 5% in Doncaster (lowest around Doncaster Hill where there are new apartments, perhaps too new to be occupied on census night?), 4% in South Yarra East (lowest in the new apartments around South Yarra Station, again possibly because some are very new) and Prahran – Windsor.

Curiously, Docklands dwelling occupancy increased by 9% from 75% to 85% (rounding means that those numbers don’t perfectly add). Perhaps there were many new yet-to-be-occupied dwellings in 2006? For reference, Dockland’s 2011 occupancy was 84%, only slightly below the 2016 level.

The outer growth areas are a mixed bag of increases and decreases. This possibly depends again on how many brand new but not yet occupied dwellings there were in 2006 and 2016.

What are the dwelling occupancy patterns in other cities?

Sydney

You can see lower occupancy around the CBD, North Sydney, Manly, and the northern beaches, and higher occupancy in the western suburbs.

The largest declines are evident in the city centre and North Ryde – East Ryde:

Brisbane

Brisbane has some big declines to the north-east of the city centre, Rochedale – Burbank, Woodridge, Logan, and Leichhardt – One Mile. The Redland Islands in the east are presumably a popular place for holiday homes.

Perth

Low occupancy is evident around Mandurah in the south (a popular holiday home area). Lower occupancy has spread around the inner city, and beach-side suburbs of Scarborough, Cottesloe, Fremantle, and Rockingham (many of which are areas with higher concentrations of Airbnb properties).

The biggest declines were in Maylands, Victoria Park – Lathlain – Burswood, and South Lake – Cockburn Central. For the first two of these areas the decline was mostly in flats/units/apartments.

Adelaide

The lowest occupancy is on the south coast and in Glenelg. The biggest decline was in Fulham (-5%), followed by Payneham – Felixstowe (-4%):

[Canberra, Hobart and Darwin added 6 November 2017]

Canberra

Dwelling occupancy was lowest around Parliament House (the census was not during a sitting week in 2016), and highest in the outer northern and southern suburbs. The 2006 census was during a sitting week, so it’s little surprise that big dwelling occupancy reductions were seen around Capital Hill between 2006 and 2016. There was also a 5% decline in Farrer and a 6% growth in Gungahlin between 2006 and 2016 (Gungahlin’s dwellings almost doubled between 2006 and 2011, so the 2006 result might reflect brand new dwellings awaiting occupants).

Hobart

Dwelling occupancy was lowest in central Hobart, with the biggest decline of 4% in Old Beach – Otago, but overall there was little change between 2006 and 2016 (average occupancy did drop slightly in 2011 though).

Darwin

Darwin dwelling occupancy was lowest in the city centre at 82% in 2016, while Howard Springs had 100% occupancy (in 2016). Declines are evident between 2006 and 2016 across most parts of Darwin.

Gold Coast

Here’s a map of 2016 occupancy at SA1 level, with the original broader colour scale:

You can see quite clearly that the beach-side areas have low occupancy, while the inland areas have much higher occupancy (some at 100%). Presumably many permanent residents cannot or choose not to compete with tourism for beach-side living.

Sunshine Coast

Similar patterns are evident on the Sunshine Coast, particularly around Noosa and Sunshine Beach in the north:

If you want to see other cities, move around Australia in Tableau for occupancy maps at CD/SA1 and SA2 geography (choose you year of interest), and occupancy change maps (at SA2 geography).

So are there lots of unoccupied inner city apartments in Melbourne?

Some commentators have spoken about many inner city apartments being unoccupied – perhaps through a glut or investors chasing capital gains and not interested rental incomes.

Here is dwelling occupancy in central Melbourne at SA1 geography for 2016, using the broader colour scale (also in Tableau):

There are quite a few pockets of very low occupancy, particularly areas shaded in yellows and greens. The average private dwelling occupancy for the City of Melbourne local government area was 87%, lower than the Greater Melbourne average of 91%.

The lowest occupancy is a block between Adderley, Spencer and Dudley Street in North Melbourne at 56%, which is probably related to the recent completion of an apartment tower not long before the census (from Google Street view we know it was under construction in April 2015 and completed by October 2016).

There are several patches of yellow (65-70% occupancy) in the CBD, Docklands and Southbank.

But what about apartment towers? For that we need to drill down to mesh blocks – and thankfully 2016 census data is actually provided at this level.

Here’s a map showing dwelling occupancy of mesh blocks in the City of Melbourne (local government area) with at least 100 dwellings per hectare (as an arbitrary threshold for large apartment building – see the appendix for an example of this density):

Some notable low occupancy apartment towers include:

48% for an apartment tower at 555 Flinders Street (Northbank Place Central Tower) between Spencer and King Street and the railway viaduct. It wasn’t brand new in 2016.

47% in a block that includes the Melbourne ONE apartment tower, possibly because it was only just opened (as I write there are still apartments for sale)

66% for a tower at 28 Southgate Ave (corner City Road), and 67% for the Quay West tower next door (almost certainly popular places for Airbnb / serviced apartments).

Several of these towers include advertised serviced apartments, and I expect the towers would contain a mix of serviced apartments, owner-occupied apartments and rentals (regular and Airbnb). However ABS advises me that field officers do speak to building managers, and are therefore likely to not code serviced apartments as private dwellings.

That said, according to the 2016 census data there were only 11 non-private dwellings in Docklands that were classified as “Hotel, motel, bed and breakfast”, and zero non-private dwellings in the New Quay apartment towers.

I snapped this picture at 9pm on a Sunday in September 2017 of the apartments at New Quay (Docklands) that at the 2016 census had 65-70% occupancy:

Of course you wouldn’t expect lights to be on in all rooms in all occupied dwellings at 9pm on a particular Sunday, but I dare say it’s probably a time when fewer people would be out. It looks like a lot less than a quarter of rooms are lit. I know very few of these are on Airbnb (more on that in a future post!), but I don’t know how many are actually serviced apartments.

There’s huge variation in dwelling occupancy across these mesh blocks. So is the lower occupancy more concentrated in higher density areas? Here’s a scatter plot of all mesh blocks in the City of Melbourne by dwelling density and occupancy:

There’s not a strong relationship between density and occupancy. The variation in dwelling occupancy between mesh blocks will probably depend on a lot of local factors.

What about occupancy by dwelling type for the inner city?

(data points removed where dwelling counts were small, the isolated blue dot at the bottom is for Southbank).

There’s no evidence that flats / apartments have lower occupancy than other housing types in the central city. However there is evidence that inner city areas have relatively lower occupancy.

So how does the occupancy of apartment blocks of 4+ storeys vary across Melbourne?

Box Hill had the lowest apartment occupancy of 50% (perhaps some were brand new?), followed by Ringwood, Glen Waverley, and Brighton in the 70-75% range. Croydon East, Templestowe , Seddon – Kingsville, Clayton, Carnegie, West Footscray, Braybrook and Frankston reported occupancy above 95%. The inner city areas were around 84-85% occupied, and these would make up the majority of such dwellings in Melbourne.

Apartments in blocks of 4+ storeys seem to have lower occupancy on average because most of them are located in the central city, which generally has lower dwelling occupancy.

Here’s a similar map (with a different colour scale) for dwelling occupancy of separate houses across the Melbourne region:

The lowest rates in metropolitan Melbourne are 82-83% in some inner city areas, while the urban growth shows up in pink and purple, mostly 94-96%.

Explore the 2016 occupancy rates at SA2 geography for different dwelling types for any part of Australia in Tableau. You can also view changes in occupancy rates since 2006 for separate houses, flats/units/apartments, and semi-detached/townhouses.

Why are there lower dwelling occupancy rates in the central city?

The census doesn’t answer this, and I’m not a housing expert, but I dare say there are plenty of plausible explanations:

Many dwellings are rented out on Airbnb (and/or other platforms) – but are not in high demand on a weeknight in mid-winter (more on that in a future post).

Many dwellings are serviced apartments that are indistinguishable from regular private dwellings (in buildings with a mixture of dwelling use). ABS say they don’t count these as private dwellings, however they are not showing up as non-private dwellings.

Dwellings are more likely to occupied by executives who travel more frequently.

Dwellings might be second homes for people living outside the city.

Dwellings might be owned by employers for interstate staff visiting Melbourne.

Dwellings might be poorly constructed and uninhabitable (eg mould issues).

Investors who are not interested in rental income might deliberately leave properties vacant (something that is disputed).

But I’m just speculating.

What about dwelling occupancy in the centre of other cities?

Here’s a map of the Sydney CBD area at SA1 geography:

There are some very low occupancy rates in the north end of the CBD, but very high occupancy rates around Darling Harbour and Pyrmont.

Here’s central Brisbane:

Here are occupancy rates for different dwelling types for selected inner city SA2s in Sydney, Brisbane, Adelaide and Perth:

In all SA2s except Surrey Hills (Sydney) and South Brisbane, flats or apartments in 4+ storey blocks had the lowest dwelling occupancy in 2016. Only in Perth City SA2 (which is quite a bit larger than the CBD) is there a reasonably clear relationship between housing type and occupancy.

Summary of findings

Couldn’t be bothered reading all of the above, or forgot what you learnt? Here’s a summary of findings:

Dwelling occupancy, as measured by the census, has declined in most Australian cities between 2006 and 2016 (particularly larger cities).

Dwelling occupancy is generally very low in popular holiday home areas, but also relatively low in central city locations.

Dwelling occupancy is generally highest in outer suburban areas.

Higher density housing types generally have lower occupancy, but that is probably because they are more often found in inner city areas.

There are examples of low occupancy apartment towers in Melbourne, but there’s not a clear relationship between dwelling density and dwelling occupancy in central Melbourne.

In a future post I plan to look more at why properties might be unoccupied, and for how long they are unoccupied, drawing on Airbnb and water usage datasets. I might also look at bedrooms and bedroom occupancy which is a whole other topic.

Appendix – About the census dwelling data

I’ve loaded census data about occupied and unoccupied private dwellings data into Tableau for 2006, 2011, and 2016 censuses for sixteen Australian cities at the CD (2006) / SA1 (2011,2016) level, which the smallest geography available for all censuses. I’ve mapped all these CDs and SA1s to boundaries of 2016 SA2s and 2011 Significant Urban Areas (as per my last post). Those mappings are unfortunately not perfect, particularly for 2006 CDs.

The ABS determine a private dwelling to be occupied if they have information to suggest someone was living in that dwelling on census night (eg a form was returned, or there was some evidence of occupation). Under this definition, unoccupied dwellings include those with usual residents temporarily absent, and those with no usual residents (vacant).

For my detailed maps I’ve only included CDs / SA1s with a density of 2 dwellings per hectare or more.

For reference, here is a Melbourne mesh block with 100 dwellings per hectare:

And here is a mesh block with 206 dwellings per hectare (note only a small part of mesh block footprint contains towers):

While journeys to work only represents around a quarter of all trips in Melbourne, they represent around 39% of trips in the AM peak (source: VISTA 2012-13). Thanks to the census there is incredibly detailed data available about the journey to work, and who doesn’t like exploring transport data in detail?

Between 2006 and 2016, Melbourne has seen mode shifts away from private transport and walking, and towards public transport and cycling. The following measures are by place of enumeration (and 2011 Significant urban area boundaries):

2006

2011

2016

Public transport (any)

14.16%

16.34%

18.15%

+2.18%

+1.82%

Private transport (only)

80.43%

78.16%

76.20%

-2.28%

-1.96%

Walk only

3.63%

3.46%

3.47%

-0.18%

+0.01%

Bicycle only

1.34%

1.56%

1.63%

+0.23%

+0.06%

This post unpacks where mode shifts and trip growth is happening, by home locations, work locations, and home-work pairs. It tries to summarise the spatial distribution of journeys to work in Melbourne. It will also look at the relationship between car parking, job density and mode shares.

I’m afraid this isn’t a short post. So get comfortable, there is much fascinating data to explore about commuting in Melbourne.

Public transport share by home location

Here’s an animated public transport mode share map 2006 to 2016 – you might want to click to enlarge, or view this map in Tableau (be patient it can take some time to load and refresh). For those with some colour-blindness, you can also get colour-blind friendly colour scales in Tableau.

The higher mode shares pretty clearly follow the train lines and the areas covered by trams, with mode share growing around these lines. Public transport mode shares of over 50% can be found in a sizeable patch of Footscray, and pockets of West Footscray, Glenroy, Ormond – Glen Huntly, Murrumbeena, Flemington, Docklands, Carlton, and South Yarra. Larger urban areas with very low public transport mode share can be found around the outer east and south-east of the city, particularly those remote from the rail network.

The biggest shifts to public transport in the middle and outer suburbs were in Wyndham Vale, Tarneit, South Morang, Lynbrook/Lyndhurst, Point Cook South, Williams Landing, Rockbank, and Glenroy. That’s almost a roll call of all the new train stations opened between 2011 and 2016. The exceptions are Rockbank (a small community at present which received significantly more frequent trains in 2015), Point Cook South (which now has buses operating every 11 minutes in the AM peak to nearby Williams Landing Station), and Glenroy (where more people are commuting to the city centre and increasingly by public transport).

Inner suburban areas with high mode shifts include West Footscray, Yarraville, Seddon – Kingsville, Collingwood, Kensington, and Brighton. The Melbourne CBD itself had a 12% shift to public transport – and actually a 7% mode shift away from walking (which probably reflects the new Free Tram Zone in the CBD area).

The biggest mode shifts away from public transport (of 1 to 2%) were at Ardeer – Albion, St Kilda East, Malvern Glen Iris, Chelsea – Bonbeach, Seaford, Dandenong, Hampton Park – Lynbrook, Lysterfield, and Monbulk – Silvan. At the 2016 census there were no express trains operating on the Frankston railway line due to level crossing removal works, which might have slightly impacted public transport demand in Seaford and Chelsea – Bonbeach. I’m not sure of explanations for the others, but these were not large mode shifts.

Public transport mode share by work location

Here’s a map showing work location public transport mode share (Destination Zones with less than 5 travellers per hectare not shown):

It’s no surprise that public transport mode share is highest in the CBD and surrounding area, and lower in the suburbs. But note the scale – public transport mode share falls away extremely quickly as you move away from the city centre.

Private transport mode shares are very high in the middle and outer suburbs:

Large areas of Melbourne have near saturation private transport mode share. In most suburban areas employee parking is likely to be free and public transport would struggle to compete with car travel times, even on congested roads (particularly for buses that are also on those congested roads).

There are some isolated pockets of relatively high public transport mode share in the suburbs, including

34% in a pocket of Caulfield – North (right next to Caulfield Station),

33% in a pocket of Footscray (includes the site of the new State Trustees office tower near the station),

And here’s a map showing the mode shift between 2011 and 2016 by workplace location:

The biggest shifts to public transport were in the inner city. The biggest shift away from public transport was Altona Meadows (but volumes were tiny – 73 journeys went down to 51).

Here’s a closer look at the inner city:

Docklands had the highest mode shift to public transport of 8.8% (almost all of it involving train) followed by Collingwood with 7.0% and Parkville with 6.1%.

North Melbourne saw a decline of 1.5% – at the same time private transport mode share and active (only) mode shares increased by 1%. Brunswick West saw a 2.3% decline in public transport mode share, a 1.2% increase in active transport and a 3.4% increase in private transport share.

Another way to slice this data is by distance from the CBD. Here are main mode shares by workplace distance from the centre, over time:

For this and several upcoming pieces of analysis, I have aggregated journeys into three “main mode” categories:

Public transport (any trip involving public transport)

Private transport (any journey involving private transport that doesn’t also involve public transport)

Active transport only (walking or cycling)

Here are the mode shifts by workplace distance from the centre between 2006 and 2016:

The biggest mode shift from private to public transport was for distances of 1-2km from the city centre, which includes Docklands, East Melbourne, most of Southbank, and southern Carlton and Parkville (see here for a reference map). A mode shift to public transport (on average) was seen for workplaces up to 40km from the city centre. The biggest mode shift to active transport was for jobs 2-4 km from the city centre (but do keep in mind that weather can impact active transport mode shares on census day).

What about job density?

Up until now I’ve been looking at mode shifts by geography – but the zones can have very different numbers of commuters. What matters more is the overall change in volumes for different modes. A big mode shift for a small number of journeys can be a smaller trip count than a small mode shift on a large number of journeys.

Firstly, here’s a map of jobs per hectare in Melbourne (well, jobs where someone travelled on census day and stated their mode, so slight underestimates of total employment density):

Outside the city centre, relatively high job density destination zones include:

Heidelberg (Austin/Mercy hospitals with 10.2% PT mode share),

Monash Medical Centre in Clayton (8.3% PT mode share),

Northern Hospital (3.8% PT mode share),

Victoria University Footscray Park campus (21.1% PT mode share),

Swinburne University Hawthorn (39.8% PT mode share),

a pocket of Box Hill (19.9% PT mode share),

a zone including the Coles head office in Tooronga (11.2% PT mode share),

an area near Camberwell station (26.8% PT mode share),

a pocket of Richmond on Church Street (27.8% PT mode share), and

a pocket of Richmond containing the Epworth Hospital (39.5% PT mode share).

You’ll probably not be very surprised to see that there is a very strong negative correlation between job density and private transport mode share. The following chart shows the relationship between the two for each Melbourne SA2 with the thin end of each “worm” being 2006 and the thick end 2016 (note: the job density scale is exponential):

Correlation of course is not necessarily causation – high job density doesn’t automatically trigger improved public and active transport options. But parking is likely to be more expensive and/or less plentiful in areas with high employment density, and many employers will be attracted to locations with good public transport access so they can tap into larger labour pools.

The Melbourne CBD SA2 is at the bottom right corner of the chart, if you were wondering.

The Port Melbourne Industrial and Clayton SA2s are relatively high density employment areas with around 90% private transport mode shares.

Here’s a zoom in on the “middle” of the above chart, with added colour and labels to help distinguish the lines:

Not only is there a strong (negative) relationship between job density and private transport mode share, most of these SA2s are moving down and to the right on the chart (with the exception of North Melbourne which saw only small change between 2011 and 2016). However the correlation probably reflects many new jobs being created in areas with good public and active transport access, particularly as Melbourne grows its knowledge economy and employers want access to a wide labour market.

How does private transport mode share relate to car parking provision?

Do more people drive to work if parking is more plentiful where they work?

Thanks to the City of Melbourne’s Census of Land Use and Employment, I can create a chart showing the number of non-residential off-street car parks per 100 employees in the City of Melbourne (which I will refer to as “parking provision” as shorthand):

Car parking provision per employee has increased in Carlton, North Melbourne and Port Melbourne and decreased in Docklands, West Melbourne (industrial), and Southbank. Docklands had the highest car parking provision in 2002 but this has fallen dramatically and land has been developed for employment usage. Southbank, which borders the CBD, has relatively high car park provisioning – much higher than Docklands and East Melbourne.

Here’s the relationship between parking provision and journey to work private transport mode share between 2006 and 2016:

It’s little surprise to see a strong relationship between the two, although Carlton is seeing increasing parking provision but decreasing private transport mode share (maybe those car parks aren’t priced for commuters?). North Melbourne increased on both measures between 2011 and 2016.

If all non-resident off street car parks were used by commuters, then you would expect the private transport mode share to be the same as the car parks per employee ratio.

Private transport mode shares were much the same as parking provision rates in Melbourne CBD, Docklands, and Southbank, suggesting most non-residential car parks are being used by commuters (with the market finding the right price to fill the car parks?). Private transport mode share was higher than car parking provision in East Melbourne, Parkville, South Yarra, North Melbourne, and West Melbourne (industrial). This might be to do with on-street parking and/or more re-use of car parks by shift workers (eg hospital workers).

Port Melbourne parking provision is very high (there is also lots of on-street parking). It’s possible some people park in Port Melbourne and walk across Lorimer Street (the CLUE border) to work in “Docklands” (which includes a significant area just north of Lorimer Street). It’s also likely that many parking spaces are reserved for visitors to businesses. Carlton similarly had higher parking provision than private transport mode share (again, could be priced for visitors).

(Data notes: For 2011, I have taken the average of 2010 and 2012 data as CLUE is conducted every even year. I’ve done a best fit of destinations zones to CLUE areas, which is not always a perfect match)

Where are the new jobs and how did people get to them?

Here’s a map showing the relative number of new jobs per workplace SA2, and the main mode used to reach them:

The biggest growth in jobs was in the CBD, followed by Docklands, and then Dandenong in the south-east.

The CBD added 33,210 jobs, and almost all of those were accounted for by public transport journeys, although 2,750 were by active transport, and only 867 new jobs by private transport (3%).

Likewise most of the growth in Docklands and Southbank was by public transport, and then in several inner suburbs private transport was a minority a new trips.

However, Southbank still has a relatively high private transport mode share of 44.5% for an area so close to the CBD. The earlier car parking chart showed that Southbank has about one off-street non-residential car park for every two employees. These include over 5000 car parks at the Crown complex alone (with $16 all day commuter parking available as at November 2017). It stands to reason that the high car parking provision could significantly contribute to the relatively high private transport mode share, which is in turn generating large volumes of radial car traffic to the city centre on congested roads. Planning authorities might want to consider this when reviewing applications for new non-residential car parks in Southbank.

Here’s a chart look looking at commuter volumes changes by workplace distance from the CBD (see here for a map of the bands).

(Note: the X-axis is quasi-exponential)

Public transport dominated new journeys to work up to 2km from the city centre and only just outnumbered private transport between 2 and 4 km. Private transport dominated new journeys to workplaces more than 4km from the city centre – however that doesn’t necessarily mean a mode shift away from public transport if the new trips have a higher public transport mode share than the 2011 trips. Indeed there was a mode shift towards public transport for workplaces in most parts of Melbourne.

Here is a map showing the private transport mode share of net new journeys to work by place of work:

Private transport had the lowest mode share of new jobs in the inner city. As seen on the map, some relative anomalies for their distance from the CBD include Hampton (70%), Brunswick East (40%), and Albert Park (24%). Explore the data in Tableau.

Where did the new commuters come from and what mode did they use?

Here’s a map showing the (relative) net volume change of private transport journeys to work, by home location:

As you can see many of the new private transport journeys to work commenced in the growth areas, although there were also some substantial numbers from inner suburbs such as South Yarra, Richmond, Braybrook, Maribyrnong and Abbotsford.

There are many middle suburban SA2s with declines. These are also suburbs where there has been population decline – which I suspect are seeing empty nesting (adult children moving out) and people retiring from work. For example Templestowe generated 561 fewer private transport trips, 48 fewer active transport only trips, but only 50 new public transport trips.

Here’s a similar map showing change in public transport journeys:

The biggest increases were from the inner city, with the CBD itself generating the largest number of new public transport trips (including almost 2500 journeys involving tram). However there were a number of new public transport trips from the Wyndham area in the south-west (where new train stations opened).

Here’s a map of the total new trip volume and main mode split:

You can see that private transport dominates new journeys from the outer suburbs, but less so in the south-west where a new train line was opened. The middle and inner suburbs are hard to see on that map, so here is a zoomed in version:

You can see many areas where private transport accounted for a minority of new trips.

Here’s how it looks by distance from the city centre:

Public transport dominated new journeys to work for home locations up until 10km from the city centre, was roughly even with private transport from 10km to 20km (hence a net mode shift to public transport). However private transport dominated new commuter journeys beyond 20km – most of which is from urban growth areas. The 24-30 km band covers most of the western and northern growth areas, while the 40km+ band is almost entirely the south-east growth areas.

Here is a view of the private transport mode share of net new trips:

(explore in Tableau)

The pink areas had a net decline in the number of private transport trips (or total trips) generated, so calculating a mode share doesn’t make a lot of sense. There are some areas with 100%+ which means more new private transport trips were generated than total new trips – ie active and/or public transport trips declined.

You can again see that private transport dominated new trips in the most outer suburbs, with notable exceptions in the west:

Wyndham in the south-west where two new train stations opened. 38% of new trips from Wyndham Vale and 30% of new trips from Tarneit were by public transport.

Sunbury in the north-west, to which the Metro train network was extended in 2012. Around 28% of new trips from Sunbury were by public transport (that’s 329 trips).

How has the distribution of home and work locations in Melbourne changed by distance from the city?

Here’s a chart showing the number of journey to work origins and destinations by distance from the city centre by year. Note the distance intervals are not even, so look for the vertical differences in this chart:

You can see most of the worker population growth (origins) has been in the outer suburbs. The destination (job) growth was much more concentrated in the inner city between 2006 and 2011, but then more evenly distributed across the city in 2016.

The median distance of commuter home locations from the city centre increased from 18.2 km in 2006 to 18.6 km in 2016. The median distance from the city centre of commuter workplaces decreased from 13.3 km in 2006 to 12.8 km in 2011 but then increased back to 13.3 km in 2016.

Here’s another way at looking at the task. I’ve split Melbourne by SA2 distance from the CBD (to create 10km wide rings) for home and work locations (and further split out the CBD as a place of work) to create a matrix. Within each cell of the matrix is a pie chart – the size of which represents the relative number of commuter trips between that home and work ring, and the colours showing the main mode. I’ve then animated it over 2011 and 2016 (to make it five dimensional!).

I think this chart fairly neatly summarises journeys to work in Melbourne:

Private transport dominates all journeys that stay more than 5km from the city centre (all but top left corner)

Active transport is only significant for commuters who work and live in the same ring (diagonal top left – bottom right), or for trips entirely within 15 km of the centre (six cells in top left corner)

Public transport dominates journeys to the CBD, no matter how far away people’s homes are, but the number of such journeys falls away rapidly with home distance from the CBD. Very few people commute from the outer suburbs to the CBD.

Private transport commuters are mostly travelling between middle suburbs, not to the CBD or even the to within 5 km of the city. However on average they are travelling towards the centre. This will become clearer shortly.

Public transport otherwise only gets 15% or better mode share for trips to within 5 km of the centre or the relatively small number of outward trips from the inner 5km.

Here’s a look at the absolute change in number of trips between the rings:

You can see:

A significant growth in private transport trips, particularly within 5 – 25 km from the CBD.

A significant growth in public transport trips, mostly to the CBD and areas within 5 km from the CBD.

Where are commuters headed on different modes?

This next analysis looks at the distribution of origins and destinations for people using particular modes, which can be compared to all journeys.

The next chart looks at the distributions of work destinations by main mode for each census year (using a higher resolution set of distances from the CBD).

On the far right is the distribution of jobs across Melbourne (with roughly equal numbers in each distance interval), and then to the left you can see the distribution of workplace locations for people who used particular modes. You can see how different modes are more prominent in different parts of the city.

You might need to click to enlarge to read the detail.

In 2016, trips to within 2km of the city centre accounted for 19% of all journeys, but 62% of public transport journeys, 31% of walking journeys, and only 7% of private transport only journeys.

Train, tram, and bicycle journeys are biased towards the inner city, while private transport only journeys are biased to the outer suburbs. Walking and bus journeys are only slightly biased towards the inner city. This should come as no surprise given the maps above showing high public transport mode shares in the inner city and very high private transport mode shares in most of the rest of the city.

Over time, public transport journeys to work became less likely to be to the central city as public transport gained more trips to the suburbs. However bus journeys to work became more likely to be in the city centre (this probably reflects the significant upgrades in bus services between the Doncaster area and city centre).

Notes on the data:

Unless a mode is labelled “only”, then I’ve counted journeys that involved that mode (and possibly other modes).

Sorry I don’t have public transport mode specific data for 2006 so there are some blank columns.

Where do commuters using different modes live?

Here’s the same breakdown, but by home distance from the city centre:

Private transport commuters were slightly more likely to come from the middle and outer suburbs. Tram and bicycle commuters were much more likely to come from the inner city. Bus commuters were over-represented in the 15-25 km band – probably dominated by the Doncaster area. Train commuters were over-represented in distances 5-25 km from the city, and under-represented in distances 35 km and beyond. Journeys by both public and private transport were more likely to come from the middle suburbs.

51% of people walking to work live within 5 km of the city centre, and the growth in walking journeys to work has been much stronger in the inner city.

Here’s a chart showing the most common home-work pairs for distance rings from the CBD for public transport journeys. It’s like a pie chart, but rectangular, larger and much easier to label (I haven’t labelled the small boxes in the bottom right hand corner):

You can see the most common combination is from 5-15 kms to 0-5 kms. This is followed by 15-25 to 0-5 kms and 0-5 to 0-5 kms.

Here’s the same for private transport only journeys:

There is a much more even distribution.

Finally, here is the same for active-only journeys to work:

This is much more polarised, with almost 40% of active transport trips being entirely within 5 km of the city centre. The second most common journey is within 5-15km of the city followed by from 5-15 km to 0-5 km.

In future posts I will look at more specific mode shares and shifts in more detail, the relationship between motor vehicle ownership and journey to work mode shares, and much more!

I hope you have found this analysis at least half as interesting as I have.

(note: this post uses data re-issued in December 2017 after ABS pulled the original Place of Work data in November 2017 due to quality concerns)

My last post looked at the overall trends in journeys to work in Melbourne, with a focus on public and private transport at the aggregate level. This post dives down to look at particular modes or modal combinations, including mode shares, mode shifts and the origins and destinations of new trips.

Train

Here’s mode share for journeys involving train by home location (journeys may also include other modes):

The highest train mode shares can be seen mostly along the train lines, which will surprise no one.

In fact, we can measure what proportion of train commuters live close to train stations. The following chart looks at how far commuters live from train stations, for commuters who use only trains, used trains and possible other modes, and for all commuters.

This chart shows that almost 60% of people who only used train (and walking) to get to work lived within 1 km of a station, and almost three-quarters were within 1.5 km. But around 8% of people only reporting train in their journey to work were more than 3 km from a train station. That’s either a long walk, or people forgot to mention the other modes they used (a common problem it seems).

For journeys involving train, 50% were from within 1 km of a station, but around a quarter were from more than 2 km from a station.

Interestingly, around a third of all Melbourne commuters lived within 1 km of a train station, but a majority of them did not actually report train as part of their journey to work.

So where were the mode shifts to and from train (by home location)?

There were big mode shifts to train around new stations including Wyndham Vale, Tarneit, Lynbrook, South Morang, and Williams Landing. Other bigger shifts were in West Footscray – Tottenham, South Yarra – East, Brighton, Viewbank – Yallambie, Yarrville, Footscray, Kensington, and Flemington (some of which might be gentrification leading to more central city workers?).

There was also a big shift to trains in Point Cook – South, which doesn’t have a train station, but is down the road from the new Williams Landing Station. Almost 28% of commuters from Point Cook South work in the Melbourne CBD, Docklands or Southbank, and most of those journeys were by public transport.

We can also look at mode shares by work location. Here is train mode share by workplace location for 2011 and 2016 (I’ve zoomed into inner Melbourne as the mode shares are negligible elsewhere, and I do not have equivalent data for 2006 sorry):

The highest shares are in the CBD, Docklands and East Melbourne. Notable relatively high suburban shares include the pocket of Footscray containing State Trustees office tower (30.7% in 2016), a pocket of Caulfield including a Monash University campus (29.5%), Box Hill (up to 19.6%), Swinburne University in Hawthorn (37.4%), and 17.5% in a pocket of Yarraville.

The biggest workplace mode shifts to train were in Docklands (+8.6%), Southbank (+5.5%), Abbotsford (+5.5%), Richmond (+5.3%), Collingwood (+5.1%), Parkville (+4.9%), and South Yarra – East (+4.8%).

Bus

Across Melbourne, bus mode share had a significant rise from 2.6% in 2006 to 3.3% in 2011, and then a small rise to 3.4% in 2016. Here’s how it looks spatially for any journey involving bus:

The highest bus mode shares are in the Kew-Doncaster corridor, around Clayton (Monash University), in the Footscray – Sunshine corridor, a pocket of Heidelberg West, around Box Hill and in Altona North. These are areas of Melbourne with higher bus service levels (and most lack train and tram services).

Here’s a map showing mode shift 2011 to 2016 at the SA2 level:

Outside the Kew – Doncaster corridor there were small mode shifts in pockets that received bus network upgrades between 2011 and 2016, including Point Cook, Craigieburn, Epping – West, Mernda, Port Melbourne, and Cairnlea.

There was also a shift to buses in Ormond – Glenhuntly, which can be largely explained by Bentleigh and Ormond Stations being closed on census day due to level crossing removal works, with substitute buses operating.

There were larger declines in Laverton / Williams Landing (where a new train station opened), Footscray, and Abbotsford.

In terms of workplaces, Westfield Doncaster topped Melbourne with 14.4% of journeys involving bus, followed by Monash University Clayton with 12.8% (remember this figure does not include students who didn’t also work at the university on census day), 13.3% at Northland Shopping Centre, and 12.3% in a pocket of Box Hill.

SmartBus

“SmartBus” services operate from 5 am to midnight weekdays, 6 am to midnight Saturdays, and 7 am to 9 pm Sundays, with services every 15 minutes or better on weekdays from 6:30 am to 9 pm, and half-hourly or better services at other times. These are relatively high service levels by Melbourne standards.

SmartBus includes four routes that connect the city to the Manningham/Doncaster region via the Eastern Freeway, three orbital routes, and a couple of other routes in the middle south-eastern suburbs. All routes are relatively direct and none are particularly short. Seven of these routes serve the Manningham region.

To assist analysis, I’ve created a “SmartBus zone” which includes all SA1 and CD areas which have a centroid within 600 m of a SmartBus route numbered 900-908. These routes were all introduced between 2006 and 2011, generally replacing existing routes that operated at lower service levels (I’ve excluded SmartBus route 703 because it was not significant upgraded between 2006 and 2016).

Here are mode shares inside and outside the SmartBus zone:

In 2006 the SmartBus zone already had double the bus mode share of the rest of Melbourne, as existing routes had relatively good service levels, including Eastern Freeway services. Following SmartBus (and other bus) upgrades between 2006 and 2011, there was a 2.5% mode shift to bus in the SmartBus zone, and a 1.3% mode shift to bus elsewhere. The SmartBus zone had a further 0.5% shift between 2011 and 2016 while the shift was only 0.2% in the rest of Melbourne.

Here’s an animated look at bus mode shares for just the SmartBus zone.

You can see plenty of mode shift in the Manningham area (where many SmartBus routes overlap), but also some mode shifts along the others routes – particularly in the south-east.

Notes:

the SmartBus zone includes overlaps with some other high service bus routes – those pockets generally had higher starting mode shares in 2006.

The orbital SmartBus routes do overlap with trains and/or trams which provide radial public transport at high service levels, negating the need or bus as a rail feeder mode (still useful for cross-town travel).

I haven’t excluded sections of SmartBus freeway running from the SmartBus zone. Sorry, I know that’s not perfect analysis, particularly along the Eastern Freeway.

Train + bus

Journeys involving train and bus rose from 1.1% in 2006 to 1.5% in 2011 and 1.7% in 2016, which is fairly large growth off a small base and represents around half of all journeys involving bus. I suspect there might be some under-reporting of bus in actual bus-train journeys, as we saw many people a long way from train stations only reporting train as their travel mode.

Here’s a map showing train + bus mode share at SA2 level. Note the colour scale is in half-percent increments:

Large increases are evident around the middle eastern suburbs (particularly around SmartBus routes), the Footscray-Sunshine corridor (which have frequent bus services running to frequent trains at Footscray Station), Point Cook (where relatively frequent bus routes feeding Williams Landing Station were introduced in 2013, resulting in 750 train+bus journeys in 2016), Craigieburn (again bus service upgrades with strong train connectivity), and Wollert (likewise).

Ormond – Glen Huntly shows up in 2016 because of the rail replacement bus services at Bentleigh and Ormond Stations at the time (as previously mentioned).

Tram

Here’s a map of tram mode shares, overlaid on the 2016 tram network (there haven’t been any significant tram extensions since 2005).

Higher tram mode shares closely follow the tracks, with the highest shares in Brunswick, North Fitzroy, St Kilda, Richmond, and Docklands.

It’s also interesting to note that several outer extremities of the tram network have quite low tram mode shares – including East Brighton, Vermont South, Box Hill, Camberwell / Glen Iris (where the Alamein line crosses tram 75), Carnegie, and to a lesser extent Airport West and Bundoora. These areas have overlapping train services and/or are a long travel time from the CBD.

Overall tram mode share increased from 4.0% in 2006 to 4.6% in 2011 and 4.8% in 2016. Here’s a map of tram mode shift 2011 to 2016 by home SA2:

The biggest mode shift was +12.6% in Docklands, followed by +9.5% in the CBD. This no doubt reflects the introduction of the free tram zone across these areas. Walk-only journey to work mode share fell 4.4% in Docklands and 7% in the CBD.

Abbotsford had a 8.5% mode shift to trams, which possibly reflects the extension of route 12 to Victoria Gardens, providing significantly more capacity along Victoria Street (the only tram corridor serving Abbotsford).

There were small mode share declines in many suburbs, although this does not necessarily mean a reduction in the number of journeys by tram.

Here are tram mode shares by workplace for 2011 and 2016:

The highest workplace tram mode shares were in the CBD, along St Kilda Road south of the CBD, Carlton, Fitzroy, Parkville, Albert Park, South Melbourne, and St Kilda.

Cycling

Cycling mode share increased from 1.5% in 2006 to 1.8% in 2011 and 1.9% in 2016. These are low numbers, but the bicycle mode share was anything but uniform across Melbourne.

Firstly here’s a map of cycling mode share by home location:

There’s not much action outside the inner city, so let’s zoom in:

The highest mode shares are in the inner northern suburbs (pockets around 25%) where there has been considerable investment in cycling infrastructure.

Here’s a chart showing the mode shift at SA2 level:

The biggest mode shift was 2.2% in Brunswick West, followed by 2.1% in South Yarra West. However aggregating to SA2 level hides some of the other changes. If you study the detailed map you can see larger mode shifts in more isolated pockets and/or corridors (including a corridor out through Footscray).

Here is the growth in bicycle trips between 2011 and 2016 by home distance from the city centre:

Significant growth was only seen for homes within 10km of the city centre. Here are those new trips mapped:

What about cycling mode shares by workplaces? I’ve gone straight to the inner city so you can see the interesting detail:

The highest workplace mode shares are in the inner northern suburbs, including Parkville (9.1%) and Fitzroy North (8.2%).

You’ll note the CBD does not have a high cycling mode share (3.8%) compared to the inner northern suburbs. But if you look at the concentration of cycling commuter workplaces, you get quite a different story:

This shows the CBD having the highest concentrations of commuter cycling destinations, although there were also relatively high densities at the Parkville hospitals and the Alfred Hospital. The highest concentration of commuter cyclists in 2016 was a block bound by Lonsdale Street, Exhibition Street, Little Lonsdale Street and Spring Street (it had a mode share of 4.3%).

However if you look at the increase in bicycle commuter trips between 2011 and 2016 by workplace distance from the city, the biggest growth was for destinations 1-4 km from the city centre:

Note: I am using a different scale for charts by workplace distance from the CBD.

How has walking changed?

Overall walking-only mode share in Melbourne as measured by the census has hardly changed, from 3.6% in 2006 to 3.5% in both 2011 and 2016. However there are huge spatial variations.

Here’s walking by home location:

The highest walking mode shares are around the central city with mode shares above 40% in parts of the CBD, Southbank, Carlton, Docklands, North Melbourne, and Parkville. Outside the city centre relatively high mode shares are seen around Monash University Clayton, the Police Academy in Glen Waverley, Box Hill, and Swinburne University in Hawthorn. Walking-only trips are very rare in most other parts of the city.

Here are walking mode shares by workplace location:

The highest walking shares by SA2 in 2016 were in St Kilda East, Prahran – Windsor, South Yarra, Carlton, Carlton North, Fitzroy, and Elwood. There were also smaller pockets of high walking mode share in Yarraville, Footscray, Flemington, Northcote, Ormond – Glenhuntly, Richmond, and Box Hill.

The biggest mode shifts away from walking were in the CBD (-7.3%) and Docklands (-4.0%), which also had big shifts to tram – probably due to the new Free Tram Zone.

Overall, the biggest increase in walking journeys was seen within 5km of the city centre:

For workplaces, the biggest growth in walking was to jobs between 2-4 km from the CBD (be aware of different X-axis scales):

Most common non-car mode

Here is a map showing the most common non-car mode in 2016*. Note the most common non-car mode might still have a very small mode share so interpret this map with caution.

*actually, I’ve not checked motorbike/scooter, taxi, or truck on the basis they are very unlikely to be the most common.

Train dominates most parts of Melbourne, with notable exceptions of the Manningham region (served by buses but not trains), several tram corridors that are remote from trains, and walking around the city centre.

The southern Mornington Peninsula is a mix of bus and walking, plus some SA1s where no one travelled to work by train, tram, bus, ferry, bicycle, or walking-only!

The next map zooms into the inner suburbs, showing the tram network underneath:

Generally tram is only the dominant mode in corridors where trains do no overlap (we saw lower tram mode shares in these areas above). In most of the inner south-eastern suburbs served by trams and trains, train is the dominant non-car mode.

If you look carefully, there are a few SA1s where bicycle is the dominant non-car mode.

In case you are wondering, there are places in Melbourne where train, tram, or walking-only trumped car-only as the most common mode. They are all on this map:

Mode with the most growth

Finally, another way to look at the data is the mode with the highest growth in trips.

Here is a map showing the mode (out of car, train, tram, bus, ferry, bicycle, walk-only) that had the biggest increase in number of trips between 2011 and 2016, by SA2:

Car trips dominated new trips in most outer suburbs (particularly in the south-east), but certainly not all of Melbourne. Train was most common in many middle suburbs (and even some outer suburbs).

Bicycle was the most common new journey mode in Albert Park (+69 journeys), South Yarra – West (+58), Carlton North – Princes Hill (+65), Fitzroy North (+150) and Brunswick West (+165).

Walking led Southbank (+1292 journeys), Fitzroy (+136), and Keilor Downs (+13 with most other modes in small decline, so don’t get too excited).

Bus topped SA2s in the Doncaster corridor, but also Port Melbourne (+187), Wantirna (+16), Kings Park (+11) and Ormond – Glen Huntly (+284 with rail replacement buses operating on census day in 2016).

Tram topped several inner SA2s but also Vermont South (+37).

Want to explore the data in Tableau?

I’ve built visualisations in Tableau Public where you can choose your mode of interest, year(s) of interest, and zoom into whatever geography you like.

The Australian census provides incredibly rich data about journeys to work, with every journey classified by origin, destination, and mode(s) of transport. So you can ask questions such as “where did workers living in X commute to and how many used public transport?” or “where did workers in Y commute from and what percentage used private transport?”, or “What percentage of people in each home location work in the central city?”.

It’s very possible to answer these questions with census data, but near-impossible to produce an atlas of maps that would answer most questions.

But thanks to new data visualisation platforms, it’s now possible to build interactive tools that allow exploration of the data. I’ve built one in Tableau Public, using both 2011 and 2016 census data for all of Australia at the SA2 geography level (SA2s are roughly suburb sized). This means you can look at each census year, as well and the changes between 2011 and 2016.

I’m going to talk through what I’ve built with plenty of interesting examples from my home city Melbourne.

I hope you find exploring the data as fascinating and useful as I do. I also hope this tool makes it easier to inform transport discussions with evidence.

Also, a warning that this is a longer post, so get comfortable.

About the data (boring but important)